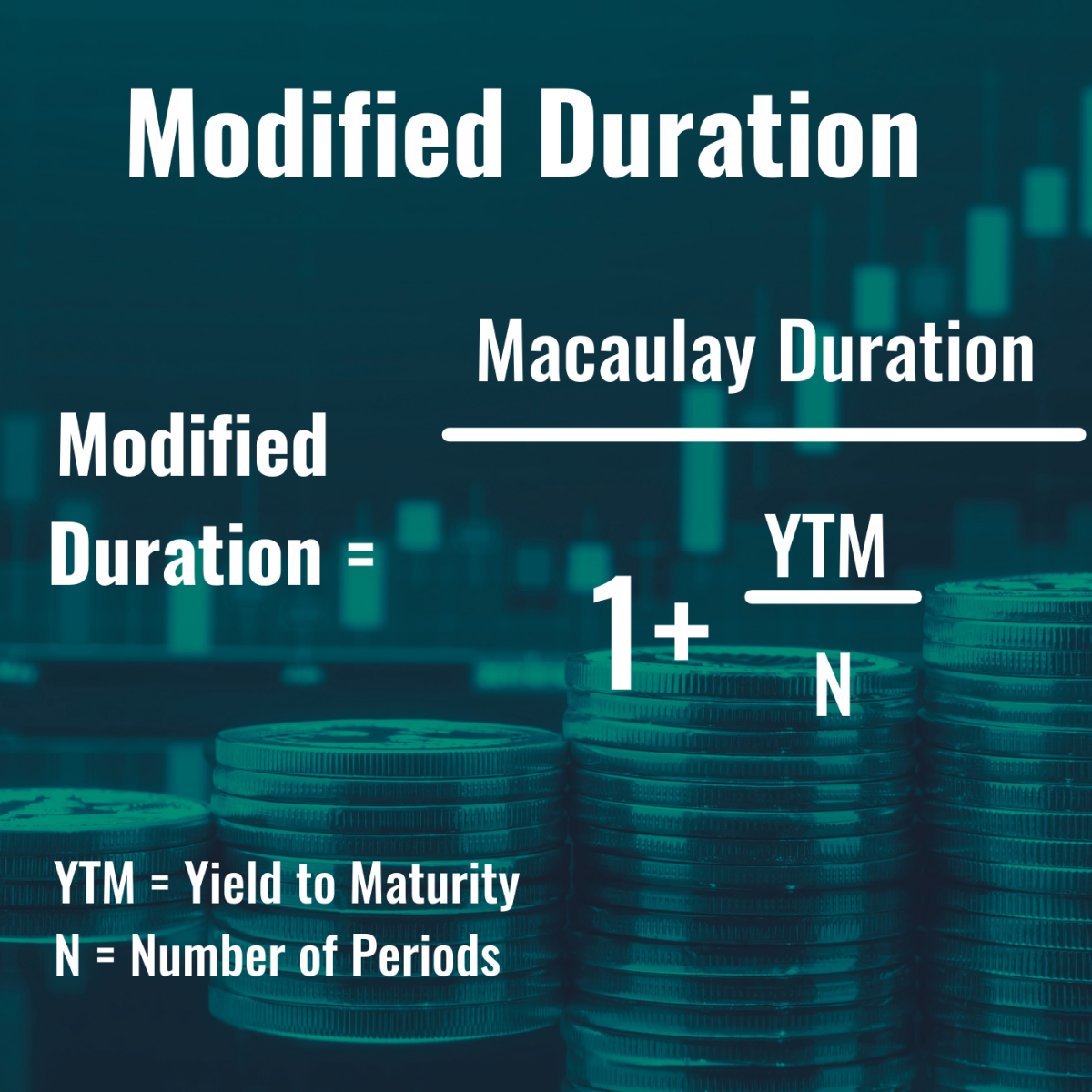

Modified Spread Duration Formula . modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. The spread duration of a portfolio is the. Spread duration is a key metric that. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. formula for spread duration.

from www.thestreet.com

modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. Spread duration is a key metric that. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. formula for spread duration. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. The spread duration of a portfolio is the.

What Is Duration of a Bond? TheStreet Definition TheStreet

Modified Spread Duration Formula Spread duration is a key metric that. Spread duration is a key metric that. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. The spread duration of a portfolio is the. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. formula for spread duration.

From www.slideserve.com

PPT Chapter 10 PowerPoint Presentation, free download ID1138614 Modified Spread Duration Formula modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. formula for spread duration. Spread duration is a key metric that. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. modified duration, a formula commonly used in bond valuations, expresses the. Modified Spread Duration Formula.

From www.investopedia.com

Key Rate Duration Definition, What It Calculates, and Formula Modified Spread Duration Formula modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. The spread duration of a portfolio is the. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. Spread duration is a key metric that. . Modified Spread Duration Formula.

From www.thestreet.com

What Is Duration of a Bond? TheStreet Definition TheStreet Modified Spread Duration Formula modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting. Modified Spread Duration Formula.

From www.slideserve.com

PPT Duration and convexity for Securities PowerPoint Modified Spread Duration Formula Spread duration is a key metric that. formula for spread duration. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. The spread duration of a portfolio is the. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a. Modified Spread Duration Formula.

From transacted.io

Spread Duration Explained Transacted Modified Spread Duration Formula This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. formula for spread duration. Spread duration is a key metric that. The spread duration of. Modified Spread Duration Formula.

From analystprep.com

Macaulay, Modified, and Effective Durations CFA Program Level 1 Modified Spread Duration Formula modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. Spread duration is a key metric that. The spread duration of a portfolio is the. formula for spread duration. modified duration is used to evaluate bond performance by comparing it against benchmarks. Modified Spread Duration Formula.

From propedia.org

Modified Duration Formula, Calculation, and How to Use It — ProPedia Modified Spread Duration Formula The spread duration of a portfolio is the. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. Spread duration is a key metric that. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. . Modified Spread Duration Formula.

From www.youtube.com

Complete illustration Duration , Modified Duration and Convexity YouTube Modified Spread Duration Formula formula for spread duration. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. Spread duration is a key metric that. The spread duration of a portfolio is the. the formula for. Modified Spread Duration Formula.

From www.educba.com

Modified Duration Formula Calculator (Example with Excel Template) Modified Spread Duration Formula modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. The spread duration of a portfolio is the. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. the formula for the modified duration is. Modified Spread Duration Formula.

From www.slideserve.com

PPT FINC4101 Investment Analysis PowerPoint Presentation, free Modified Spread Duration Formula The spread duration of a portfolio is the. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. modified duration is used to evaluate bond performance by comparing it. Modified Spread Duration Formula.

From www.slideserve.com

PPT Bond Duration PowerPoint Presentation, free download ID2987215 Modified Spread Duration Formula modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. The spread duration of a portfolio is the. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. Spread duration is a key metric that. formula for spread duration. the formula for. Modified Spread Duration Formula.

From www.financestrategists.com

Modified Duration Meaning, Formula, Applications, & Limitations Modified Spread Duration Formula formula for spread duration. The spread duration of a portfolio is the. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. Spread duration is a key metric that. This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. modified duration, a. Modified Spread Duration Formula.

From www.researchgate.net

Macaulay's Duration Model and Modified Duration Model calculation Modified Spread Duration Formula The spread duration of a portfolio is the. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. This measure helps investors understand the sources of their portfolio's performance, including. Modified Spread Duration Formula.

From www.pzacademy.com

spread duration有问必答品职教育 专注CFA ESG FRM CPA 考研等财经培训课程 Modified Spread Duration Formula This measure helps investors understand the sources of their portfolio's performance, including the impact of interest rate changes. formula for spread duration. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. modified duration is used to evaluate bond performance by comparing. Modified Spread Duration Formula.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Modified Spread Duration Formula formula for spread duration. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. This measure helps investors understand the sources. Modified Spread Duration Formula.

From www.educba.com

Modified Duration Explanation, Example with Excel Template Modified Spread Duration Formula modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. Spread duration is a key metric that. The spread duration of a portfolio is the. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. modified duration, a formula. Modified Spread Duration Formula.

From www.youtube.com

What is Duration & Modified Duration? Macauley Duration & Modified Modified Spread Duration Formula the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. modified duration is used to evaluate bond performance by comparing it against benchmarks and conducting attribution analysis. formula for spread duration. The spread duration of a portfolio is the. Spread duration is a key metric that.. Modified Spread Duration Formula.

From www.slideserve.com

PPT Bond Duration PowerPoint Presentation, free download ID2987215 Modified Spread Duration Formula Spread duration is a key metric that. modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. the formula for the modified duration is the value of the macaulay duration divided by 1, plus the yield to maturity,. formula for spread duration.. Modified Spread Duration Formula.